Last year, I remembered that I think most books are too long. Perhaps one sensible response to this is to favor reading shorter books in general. So I sorted my Goodreads to-read list after length, and started picking books from the shortest. One of those that came up was a heterodox economics book by Steve Keen called Can We Avoid Another Financial Crisis? (AA). It’s from 2017 which can be seen as a benefit since it gives some time for any predictions to have been perhaps confirmed or disconfirmed.

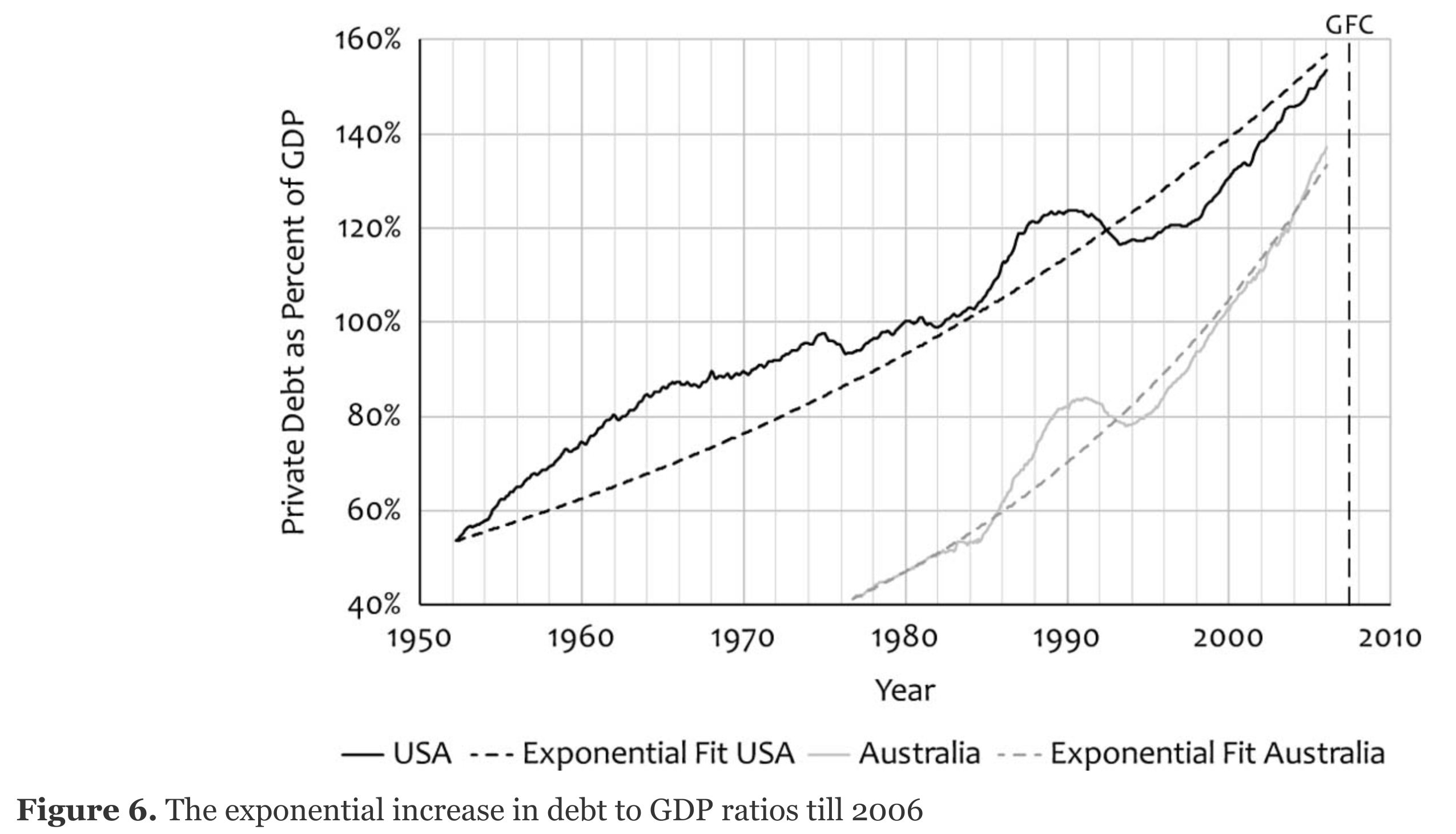

The main thesis of the book is that private debt to GDP ratio is causal for economic crises. He has some plots like this:

He thinks it’s important that one can fit an exponential model here and get a correlation of 0.97, but given such line go up charts, one can fit whatever model and get almost the same results.

The secondary thesis is that mainstream award-winning macro-economics is a poor science. The latter can be true without the former being true, of course. He spends a number of pages quoting various mainstream economics about their methods:

Minsky’s theory is compelling, but it was ignored by the economics mainstream when he first developed it, because he refused to make the assumptions that they then insisted were required to develop ‘good’ economic theory. Bernanke’s treatment of Minsky in his Essays on the Great Depression is the classic illustration of this. This book collected the papers on which Bernanke based his claim to be an expert on the Great Depression – and therefore the ideal person to head the Federal Reserve. A dispassionate observer might have expected Bernanke to have considered all major theories that attempted to explain the Great Depression, including Minsky’s. Instead, this is the entire consideration that Bernanke gave to Minsky in that book: ‘Hyman Minsky (1977a) and Charles Kindleberger (1978) have in several places argued for the inherent instability of the financial system, but in doing so have had to depart from the assumption of rational economic behavior.’ A footnote adds: ‘I do not deny the possible importance of irrationality in economic life; however, it seems that the best research strategy is to push the rationality postulate as far as it will go’ (Bernanke, 2000, p. 43).

This is the central rationality + self-interest assumption used in many models, typically called homo economicus. It’s of course a fiction, since no one really thinks humans act that way. Nevertheless, humans are largely rational we might say. They try to act on reasons for doing this or that, they try to pick the best methods for reaching their goals etc. They may fail to be optimally rational, but they are also working under various time and computation constraints, so-called bounded rationality. Humans are generally self-interested (you work for pay, not for free) but not entirely so, since they also give money to others. The receivers are mainly family, but also occasionally to strangers (even in other countries). The least self-interested thing they do is voting for large-scale welfare taxation which almost entirely benefits strangers for a large proportion of the working population (e.g. socialized healthcare is heavily used by a small minority and working age people rarely use it). Nevertheless, if we think of all the money a given person acquires in their life, most of it will be spent on themselves and their close relatives. So, maybe one can to some degree approximate human behavior in aggregate by the simplified homo economicus. I think the main reasons that economists go for these extreme assumptions is that they enable them to derive formal proofs for this or that theorem. When assumptions are made more realistic (that is, given up), it is generally not possible to deduce much from them. Many economists act as if economics has a strong mathematical foundation based on these models (micro-economics), and that economics isn’t just another social science with somewhat smarter and less politically biased practitioners. In general, I am not really well-read in macro-economics, so my review of this book probably reflects that. One key claim of Keen is that the standard models used don’t actually predict the existence of economic crises:

Working completely outside the mainstream, and with his interest in finding out whether another Great Depression could happen, Minsky began with a sublime and profound truth: to answer the question of whether another financial crisis is possible, you need an economic model that can generate a depression: ‘To answer these questions it is necessary to have an economic theory which makes great depressions one of the possible states in which our type of capitalist economy can find itself’ (Minsky, 1982, p. xi). Mainstream models – especially DSGE models – could not do this: their default state was equilibrium rather than crisis, they were assumed to return to equilibrium after any ‘exogenous shock’, and they lacked a financial sector. So Minsky had to develop his own theory, which he christened the ‘Financial Instability Hypothesis’, and it led him to his conclusion that capitalism ‘is inherently flawed’.

This is weird because those are a regular occurrence, and any model that doesn’t include these would be missing important facts of life. It would be like climatic models that fail to predict ice ages.

On another assumption that Keen has issues with:

The first economist to derive this result, William Gorman, argued that it was ‘intuitively reasonable’ to make what is in fact an absurd assumption, that changing the distribution of income does not alter consumption: ‘The necessary and sufficient condition quoted above is intuitively reasonable. It says, in effect, that an extra unit of purchasing power should be spent in the same way no matter to whom it is given’ (Gorman, 1953, pp. 63–4, emphasis added). Paul Samuelson, who arguably did more to create Neoclassical economics than any other twentieth-century economist, conceded that unrelated individual demand curves could not be aggregated to yield market demand curves that behaved like individual ones. But he then asserted that a ‘family ordinal social welfare function’ could be derived, ‘since blood is thicker than water’: family members could be assumed to redistribute income between themselves ‘so as to keep the “marginal social significance of every dollar” equal’ (Samuelson, 1956, pp. 10–11, emphasis added). He then blithely extended this vision of a happy family to the whole of society: ‘The same argument will apply to all of society if optimal reallocations of income can be assumed to keep the ethical worth of each person’s marginal dollar equal’ (1956, p. 21, emphasis added).

Maybe I am not understanding correctly what they mean, but it’s rather obvious that income distributions change consumption patterns. If you are living on the brink of starvation, you don’t buy a luxury car. This is something you consider once you are already living a decent life and wondering what to do with the excess money. Similarly, the % breakdown of spending changes with the distribution. For people living off the land with no excess income (including in goods), essentially 100% of their marginal income is spent on food. But humans can only eat so much, and food price doesn’t scale linearly with quality, so there’s little reason to spend 5000 USD a month on food as opposed to 1000 USD (or whatever your standard is). As incomes rise, thus a larger % of income is spent not on food but other stuff, a nicer house, and especially entertainment. Those comments from economists about how people would spend their money sound basically like family-wide utilitarianism, or even society-wide.

After arguing that Margaret Thatcher was responsible for Britain’s financial crisis (of 2008), he goes on to make some predictions for other countries:

A similar fate is likely to befall the new prime ministers of Canada and Australia, Justin Trudeau and Malcolm Turnbull. Both countries will suffer a serious economic slowdown in the next few years, since the only way they can sustain their current growth rates is for debt to continue growing faster than GDP, as it is doing now: a 3.8 per cent annual growth rate for Canada and 5.7 per cent for Australia, versus nominal GDP growth of zero in Canada and 2 per cent p.a. in Australia. This could happen, especially in Australia where its Central Bank could entice more leveraged property speculation, by dropping official interest rates from their outlier level of 1.5 per cent p.a. to the near zero rate that applies in most of the OECD. But a continuation of this trend is highly unlikely, for two reasons.

Firstly, if the trend continues, then both countries will have private debt to GDP ratios that exceed 250 per cent by 2020. This would be the highest level ever recorded in major OECD economies, and smaller only than tiny Luxembourg and the peculiar vassal state of Hong Kong.

Secondly, the corporate sectors of both countries are likely to reduce their debt levels strongly in the next few years, since the China-motivated minerals boom in both countries is now over. This corporate sector deleveraging will counteract any rise in household leverage, so that the required increase in household leverage to sustain their bubbles becomes simply unthinkable. For example, if the corporate debt ratio merely stabilised, then Canadian household debt would need to rise from 96 per cent to 143 per cent of GDP by 2020 to compensate. Australia, which already has the highest household debt ratio in the world of 125 per cent of GDP, would need to reach 170 per cent. That simply isn’t going to happen.

Consequently, both countries are very likely to suffer a severe economic crisis before 2020 – and possibly as early as 2017. This crisis will be blamed on the incumbents and the economic policies they follow – and in Canada’s case, it will mean that Trudeau’s decision to run a government deficit, which he flagged during the electoral campaign, will be blamed for the crisis.

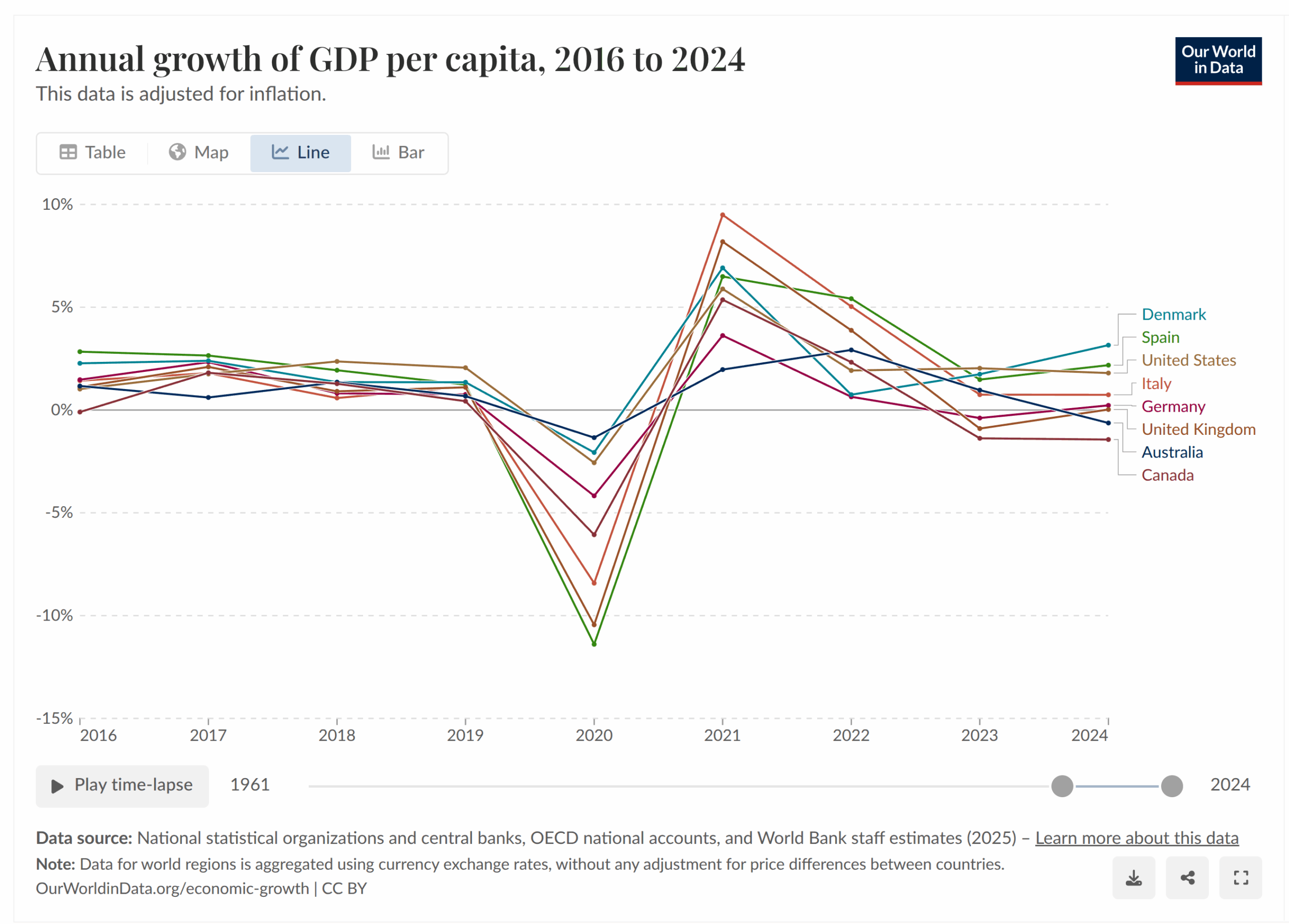

Alright, unfortunately for his predictions, we got a big COVID economic crisis at the same time, so it’s hard to say if these countries would have had some crisis without that. But we can look at whether they had unusually large declines in GDPpc growth:

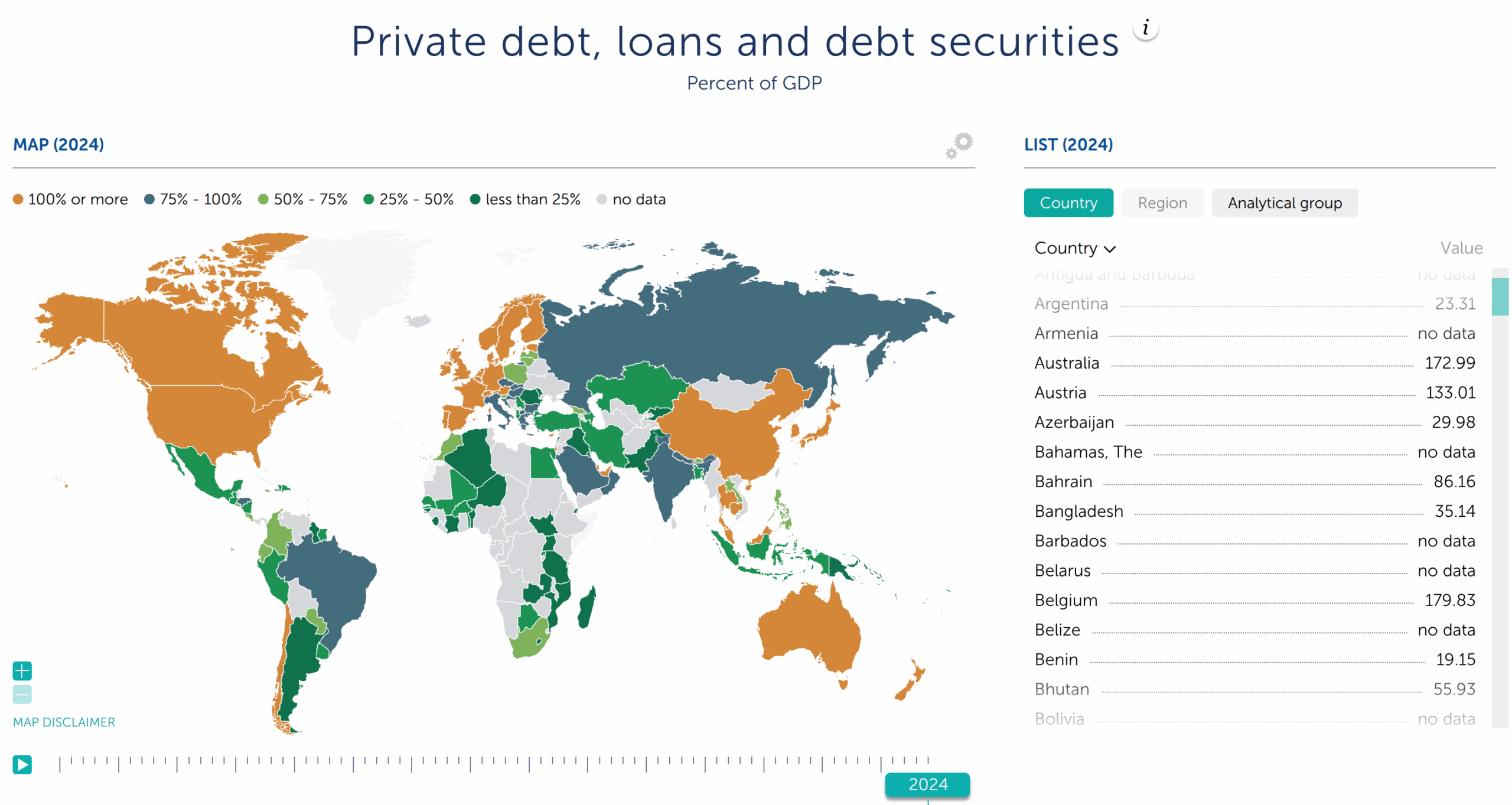

Australia had the smallest COVID decline (zero COVID policy being a mostly cut-off island), and Canada was middle of the pack. There doesn’t seem to be anything in particular about their recent economic growth that stands out with the comparison countries I’ve chosen (you could choose others). OK, but maybe we need to look at his favorite indicator, the one he says the mainstream is mostly ignoring. I sort of believe him because I’m unable to find any nice, easy to download datasets of this. This website lists the current values, but for the historical values, it seems one has to access each country’s page (e.g. Germany), so I would have to do some scraping to get the time series. WorldBank has a database for “Outstanding domestic private debt securities to GDP (%) (GFDD.DM.03)”, which sounds about the same, but the values don’t match the ones he plots. Not to be confused with the usual debt to GDP datasets, which are based on government debt. Finally, I found an IMF database, which gives us this map:

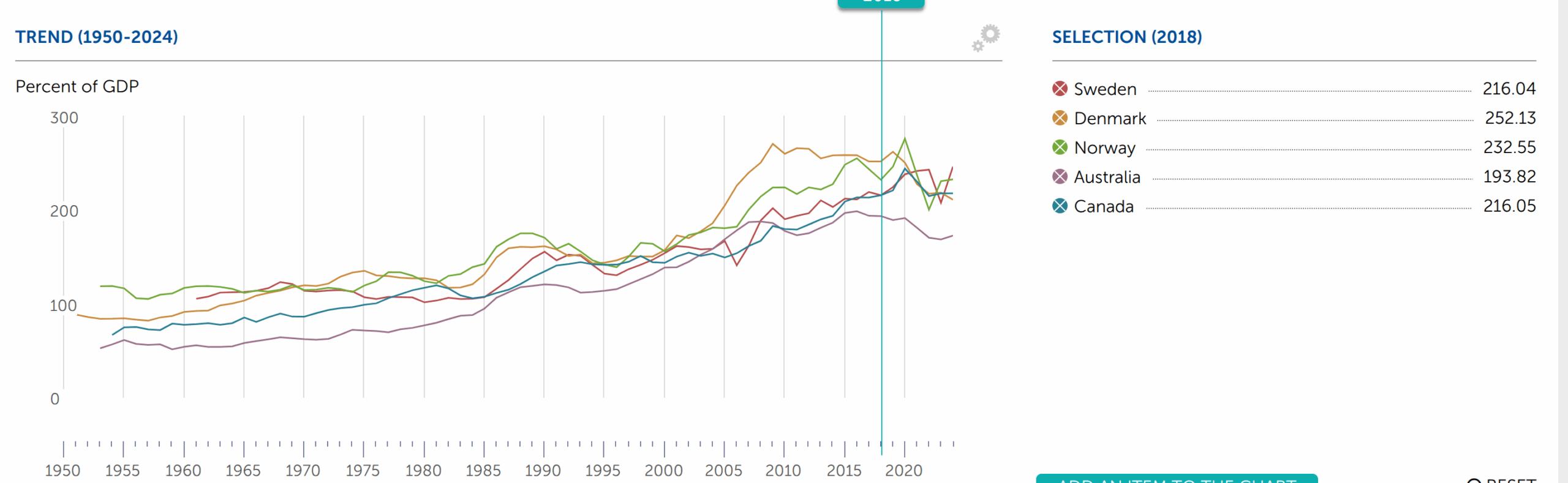

Based on simple reasoning about private debt to GDP being particular important, it seems like Scandinavia is ripe to fall, since all 3 of them have over 200% private debt of GDP and growing:

Australia and Canada don’t seem to be unusually bad on this metric, despite the current talk about the housing crisis (immigration caused).

So what does he think we need to do?:

If neither market nor indirect government action is likely to reduce private debt sufficiently, the only options are either a direct reduction of private debt, or an increase in the money supply that indirectly reduces the debt burden. Among the handful of researchers to have correctly identified private debt as the key problem afflicting the global economy today (Bezemer, 2011a; Hudson, 2009; Keen, 2014; King, 2016; Mian & Sufi, 2015; Schularick & Taylor, 2012; Turner, 2016; Wolf, 2014; see also Bezemer, 2010), Mian and Sufi (2015, ch. 10) have advocated direct debt forgiveness, while Wolf (2014), Turner (2016) and King (2016) have proposed what is colloquially described as ‘helicopter money’ – the use of the Central Bank’s capacity to create money to inject money directly into personal bank accounts.

Both proposals on their own face legitimate objections. Debt forgiveness appears to favour debtors over savers – and negative reactions to this prospect during 2009 played a large role in the rise of the Tea Party in the USA (Mian & Sufi, 2015, ch. 10). ‘Helicopter money’ doesn’t have this drawback, but it doesn’t necessarily reduce the level of private debt either: it simply dilutes the effect of outstanding debt by increasing the money supply. The scale of the injection that would be needed to bring private debt back to a level where a credit slowdown doesn’t cause a crisis – something well under 100 per cent of GDP – is also enormous.

I suggest a melding of the two approaches, in what I have called a ‘Modern Debt Jubilee’:1 make a direct injection of money into all private bank accounts, but require that its first use is to pay down debt. Debt would thus be directly reduced as with Mian and Sufi’s proposal, but debtors would not be rewarded relative to savers.

Can’t say I am in favor of this, even though I agree it’s bad that debts are rising (if I was the king, I would immediately try to reduce the country’s debt to 0 so as to avoid losing money unnecessarily to debt interests). Any kind of debt forgiveness rewards people for burrowing money carelessly, and thus punishes those who were money-wise. This is a mere moral claim of unfairness, but if governments started regularly forgiving private debts or printing money to pay it off, then surely people would just start taking on more debts. This is rather obvious and I don’t see how this ends well.

But ultimately, he is pessimistic, as these heterodox economists usually are:

So, to answer the question this book poses, no, we cannot avoid financial crises in the Debt-Zombies-To-Be, because the economic prerequisites of excessive private debt and excessive reliance on credit have already been set. Nor can we avoid stagnation in the Walking Dead of Debt, so long as we ignore the private debt overhang that is its primary cause.

We could dramatically lessen the impact of these crises if political leaders and their economic advisers understood how they are caused by credit bubbles, and we could escape stagnation if they were willing to use the State’s money-creating capacity to reduce the post-crisis overhang of excessive private debt. But because they are not, crises in the Debt-Zombies-To-Be are inevitable between now and 2020, and the plunge in their credit-based demand will take what little wind remains out of the sails of global commerce. Stagnation at the global level will be the outcome, not because of an absence of new ideas from scientists and engineers, as ‘secular stagnation’ devotees assert, but because mainstream economists have clung to delusional ideas about the nature of capitalism, even as the real world, time and time again, has proven them wrong.

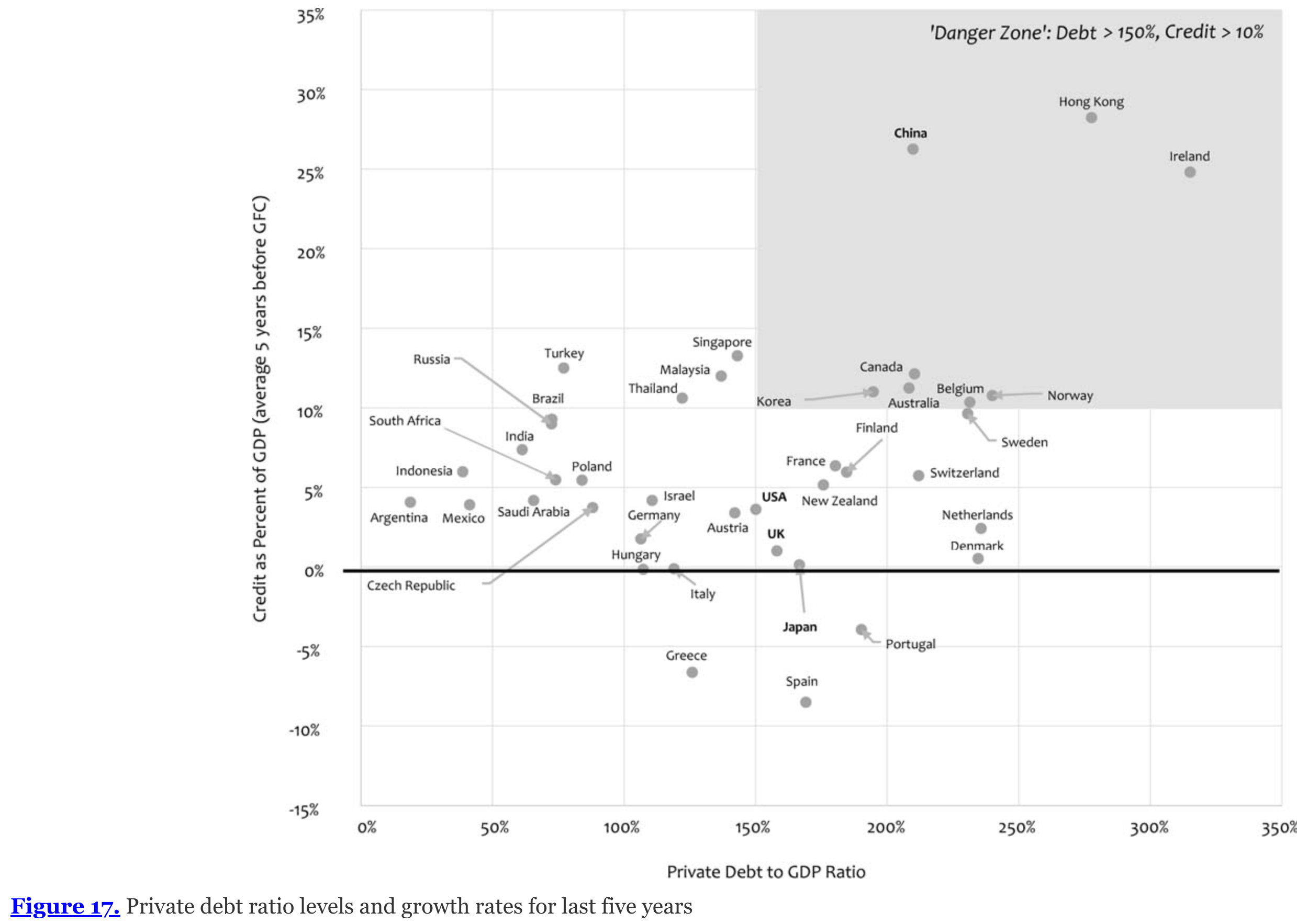

For reference, these are the zombies he is talking about:

If I had to make predictions of the future of economies, I might include debt as a useful metric (e.g. Greece has a bad government debt to GDP), but I wouldn’t think it’s the only thing that matters. That’s the impression I get from this book. I don’t really see any strong evidence that this is the case, but he says some academics agree with him (cited in the above quote), so I guess the interested reader could check out those articles and report back.